How to BRRRR Your Way To Financial Freedom

Brrrr is a HOT topic... but for good reason. This real estate investing strategy has dramatically changed the lives of millions of people. If financial freedom is the goal, AKA living off passive income, then the Brrrr strategy is likely a method you'll be using. Let's jump straight in...

What is the Brrrr method:

The Brrrr Method is a real estate investing strategy—typically single-family houses but can be used for any asset class— that beginners can do, and utilizes one large capital investment that you can "recycle" over again in 2-6 months' time for more purchases. The acronym stands for: Buy a property, then Rehab that same property, then Rent, then Refinance, and finally Repeat the process with that original capital investment. Here's a video from Sam Primm of "SamFasterFreedom" showing what a Brrr looks like from beginning to end:

Using the Brrrr Method is one of the easiest ways to get started in real estate investing because it’s not complex and it enables you to recycle your initial investment over and over again. The cornerstone that makes it work. Refinancing is the key to making this strategy work. With your ability to refinance, you can pull your capital out (or the majority of it), and recycle it into another property, exponentially growing your wealth. A problem is though that refinancing costs money. There are expensive “closing costs” associated; you have to pay escrow (or closing attorney), and the title company. In order to pay for those costs, it’ll either be out of your own pocket, or via the equity you created because you rehabbed the property (therefore adding value), and/or when you bought it at a discount. When you add value to a property, you create enough buffer to pay for those closing costs right away. Without your ability to refinance right after you’ve bought it and fixed it up, your initial investment becomes “stagnant” and you’ll have to wait until the house appreciates enough to afford closing costs and pull your investment out (which can take a couple of years or more). Let's go over some "Pros and cons" of using this method...

Pros and cons:

Pros:

- You can grow a big portfolio in a short amount of time... On average, if you do 1 deal every 4 months, you'll have 15 properties in 5 years! And you can even do it faster than that rate. See this video on Thach Nguyen on how to buy 10 Brrrr method properties in 5 years:

- It's the easiest method for wealth creation and cash flow... You don’t have to learn about the nuances of apartment investing or start a business. You can add tens of thousands of dollars to your equity in a few months AND add a new income stream almost overnight.

- No need to have millions of dollars... You just need one lump sum to get started. You don't need millions of dollars to start your empire of properties because, with the Brrrr method, you recycle your initial investment over and over again.

Cons:

- You need a large source of capital to begin with, or use creative finance (which is a somewhat advanced buying strategy that'll we'll briefly cover later)

- You’ll need to manage a rehab project... Which takes some skill set or reliance on an expensive general contractor

- You still have to qualify for a cash-out refinance loan to pull your capital out. Just because this is an investment, banks don't see it that way. When it comes to SFRs, they want to make you can afford the mortgage.

Going off market

When trying to buy a good deal on the MLS, the obstacle you’ll come across is not just competition but also the cost of purchase. You will pay a significant amount more when you buy "on-market" properties. This cuts into your equity and costs. That's why with Brrrr, it's far better to find discounted properties. There are a few ways to do this:

- Develop a network where people bring your deals — This obviously takes time but, once you get traction, you'll have a good percentage of deals coming from referrals or agents who have problem properties and want your help. There are a number of agents who are really hustling to get more real estate listings and/or using real estate social media marketing to find good discounted deals for you. Network and get to know as many as you can.

- Buy from wholesalers — A number of wholesalers are in the field using a number of techniques to find off-market deals. Anything from using handwritten mailers to cold calling to door knocking. Either way, they are finding them for you. If you get on enough wholesalers' "cash buyers" lists you'll come across a good deal.

- Directly from sellers — Marketing and advertising directly to sellers to buy their house. You'll often be targeting houses that need work or "problem situations" where the only solution for the seller is a discount cash offer. There are a number of marketing techniques, what we specialize in at Ballpoint Marketing is direct mail for real estate investors

Although trying to find motivated sellers and talking with them, might seem daunting, it has a huge payoff once you get it down because you can control your deal flow and control which properties you want and don’t want. For example, if there’s a specific area or neighborhood that you’d love to own in… you can regularly farm and market that area to find sellers who’ll directly sell their property to you at a discount (since you’re paying cash) and cut out the realtor costs. Off-Market vs "On-Market". There are a lot of articles and info on the Brrrr Strategy. Most of them center around finding a property on the MLS (aka "on-market"). However, exclusively using the MLS to buy FULL retail, you'll find that's not only very risky but you'll be hard pressed to find a good deal. That's why recommend going "off-market" as much as possible to find your Brrrr deals. We'll cover what it means to "find off-market" deals... But first, to give you an idea of how off-market can be significantly better for doing the Brrrr method... here are some number breakdowns to compare:

Deal #1 found on the MLS

- P.P (purchase price) = $300,000

- ARV = $320,000

- Repairs = $20,000

- Net Equity = $0

- Total all in (after refinance)= $70,000

Deal #2 found off-market

- P.P. = $220,000 (75% of ARV minus repairs)

- ARV = $320,000

- Repairs = $20,000

- Net equity = $80,000

- Total all in (after refinance)= approx. $10,000 (the closing costs)

... With deal #2 you have a 25% buffer, while with Deal #1 you have NO buffer and any mistake will put you above what the house is worth. ... With deal #2 you use a lot less money AND you have a lot less money stuck in the deal. .... With Deal #2 if you overpaid and/or over-budgeted you have some "wiggle room" to still sell it and make money, while with Deal #1 if you over budget you're only out is a loan and take a loss. We hope that convinces you that when you go off-market not only do you SAVE a ton more money, but you off-set your risk dramatically. Finding off-market deals may seem daunting, and we'll show you some ways to find off-market deals, but we have this guide that may help:

How to buy a Brrrr property

The first step to our strategy is buying it right. This is the part where most people get analysis paralysis and never take action with. And that’s because it’s the most daunting and risky step. There are so many factors to look into, and your friends and family (who don’t know a thing about REI or the Brrrr method) are probably playing “armchair investor” telling you that it’s not a good time to buy. Is it a good time to buy? For those that are “waiting on the right time,” I will say this: building a portfolio of cash-flowing properties is a lot like planting a tree.

The best time to do it was ten years ago, the second best time is now.

No matter the cycle of real estate… you're going to have friends and family say to you, “It’s not a good time to buy”. Don’t listen to the naysayers. It’s impossible to time the market. That’s why you need to practice Dollar-Cost-Averaging. That means that you are consistently buying properties at a discount using the Brrrr method, year-in, and year-out. Just like stocks, you don’t just buy once and hope for the best… you buy when it’s high and low; Because you can’t time things. Fortunately, real estate has far less dramatic upswings and downswings than stocks, so your dollar-cost-averaging looks much better. If you buy now, then 5 years from now you’ll be “light years” ahead of those who have been “waiting for the right time”; You’ve already planted your tree and have a few properties under your belt (no matter the cycles). Alright, let's jump into how to buy using the Brrrr method…

"Buying Formulas"

I want to give you a list of “buying formulas”. Because the numbers HAVE to pencil when you buy. Or else you’ll lose money.

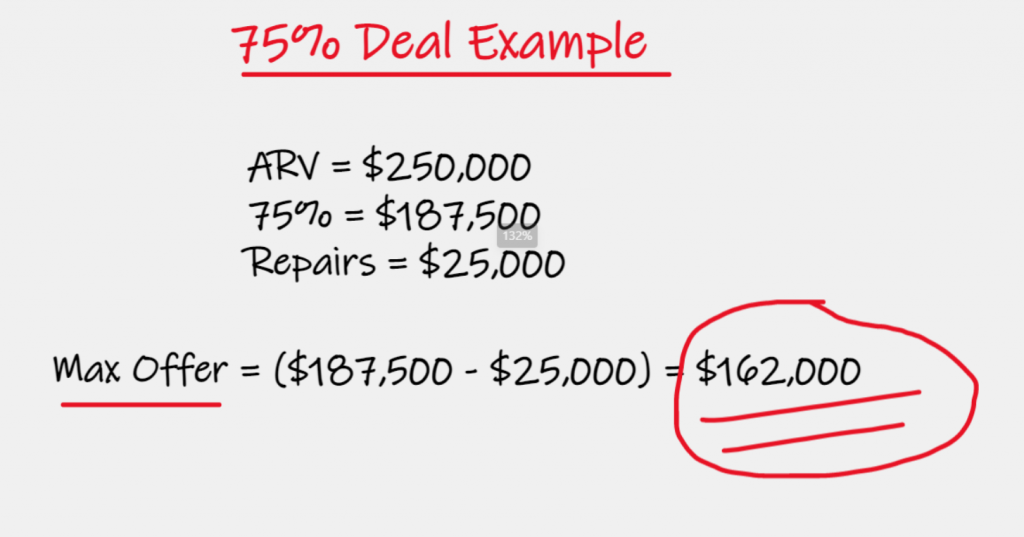

75% seems to be the “magical” number that many people quote. It works for most markets. Here’s the gist of it… You take the ARV (after repair value — what will the property be worth after you fix it up), then you take 75% of what that value is, then subtract the repair costs from it…And that's your MAX allowable offer (MAOP). Here’s an example:  However, that price doesn’t add on maintenance and other soft costs so many investors tack off $5,000 from it. So, according to that example above, if you subtract $5,000 you’re NEW MAOP (Max Allowable offer) will be:

However, that price doesn’t add on maintenance and other soft costs so many investors tack off $5,000 from it. So, according to that example above, if you subtract $5,000 you’re NEW MAOP (Max Allowable offer) will be:

$157,000

Cons of the 75% rule This is a great rule for flipping. But this alone doesn’t do justice when you’re HOLDING the property because it doesn't account for rental costs/income which is one of the main components of the Brrrr strategy; in other words, 75% rule doesn’t take into account how much cash flow (or lack of cash flow) you’ll be getting. If cash flow is important for you (which is for most investors doing the Brrrr strategy), then you’ll have to also consider how much rental income will be. The second problem with this strategy is you could be pricing it too low, and LOSING deals if you’re in a competitive market. For example, if you’re in a very competitive market AND the market is on an upswing, a 75% offer might look much lower than all the wholesalers who are giving an 80% offer or higher. The best strategy with the 75% rule? The 75% rule assures that you minimize your risk of a deal by buying at a discount and leaving a buffer if any mistakes are made. But like mentioned earlier, it doesn't account for cash flow. So, use BOTH: make sure that a deal pencils out in the 75% rule, AND make sure that it cash flows. Adjust the 75% rule As mentioned earlier... if you're in a competitive market, 75% offers might seem very low. So if you're making LOTS of offers (30+) and you still haven't gotten any bites, then adjust up your offer amount from 75% to maybe even 80% -- as long as you have a buffer and the property cash flows.

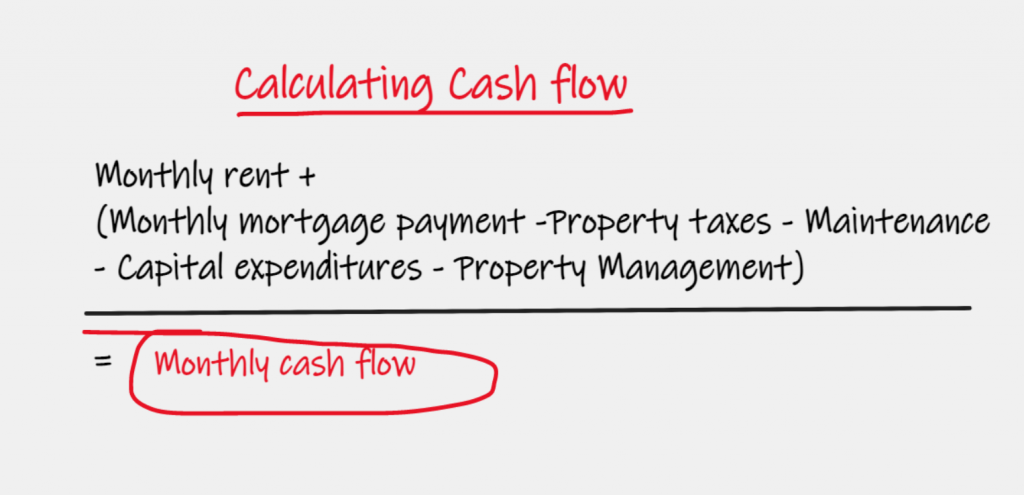

Calculating Cash Flow

Do not make the mistake that most people make... and that's thinking that cash flow = "Mortgage - Rent". If you calculate your "cash flow" in that manner, in 5 years or less, you'll loss all your "cash flow" when you have to pay for new carpet or a water heater that busted. Cash flow is calculated as follows:  So as you can see, you have not just a monthly mortgage payment to subtract but a number of other expenses like:

So as you can see, you have not just a monthly mortgage payment to subtract but a number of other expenses like:

- Property taxes (every year county will send a bill(s))

- Maintenance (wear and tear is a real expense. You'll get calls to fix things like water faucets or light bulbs)

- Capital expenditures (when a water heater goes out hopefully you've kept a reserve for big expense items like roofs, flooring, etc)

- Vacancies (It cost money to lose a tenant and put a new one back in)

- Property management (even if you're doing this yourself, it still costs money via your time. So might as deduct a certain amount and make sure you're either praying yourself or at least have a margin for management built-in in case you decided to hire this out)

As you can see.... holding a property is pricey. So you want to make sure you have that calculated out. Some people rely on a "raw cost" formula or rule of thumb like "40% of rental income goes into rental expenses" Here's a neat video showing you how to analyze cash flow: We've spent a lot of time on the "Buy" portion of the Brrrr deal because buying right is the most important aspect to this:

You make your money when you buy.... you get PAID when you sell or rent

If you buy right, all the other steps of the Brrrr strategy fall into place fairly easily. If you buy it wrong... it doesn't matter how well you rehab it, or rent it out, you might have gotten a bad deal. So let me finish this section and talk about what else to look for in buying a Brrr deal

Location

It's better to buy the ugliest house in the best neighborhood than the prettiest house in the worst neighborhood. A good deal doesn't only come down to numbers. You might be able to find "great" deals in "war zone areas" (the kind of areas where you might have to come armed or with police escort), but just because the numbers make sense, doesn't make it a good deal! (There are people who make businesses out of buying in war zones, but we won't cover that in this article) Instead, understand that the location is going to greatly affect your Brrrr deal in the areas of:

- Maintenance (Bad areas may attract bad tenants and therefore cost more in maintenance fees)

- Appraisal value (A low appraisal value can ruin your Brrrr plans. A mistake people make is comparing prices of their property in a bad area, to prices of properties in good areas.)

- Vacancies (the more turnover of tenants you have, the higher your annual costs)

- Overall headaches (bad areas attract sketchy people where drug deals and crimes are happening right in front of your neighborhood. This lowers value, increases vacancies, and makes your work harder)

So when looking for you next Brrrr deal for sake of ease and long-term costs and values... pick a desirable area. When with:

- Good schools

- Increasing values

- More homeowners than rentals

- Convenience (close to shopping and highways)

How to Rehab your Brrrr deal

How important is rehab? To hit your desired appraisal value (so that you can refinance) you gotta make sure the After Repair Value reflects your desired appraisal value; AKA you rehabbed just right. Too much and you've overspent on the rehab. People think the more money you put into rehab, the higher the value goes up. Wrong. Houses don't work that way. House prices are contingent on what the market is paying for it; AKA: how much the neighbor with the same model as your sold their house for last week, not how much money you put into. A buyer doesn't care how money you spent. Typically, they just care about the condition (that it's reasonable), and whether they can afford it or not. Just because you put a kitchen that is $20,000 more than your neighbors, doesn't mean that a buyer is going to pay that much more for it. You have to be realistic with your rehabs. Yes, do a good job. But be reasonable. Don't go out and buy the higher grade laminate floor when the lower grade suits the market just fine and you can save $5k+. Don't go and replace the ducting if it doesn't need it. Rather than replacing a whole fence, see if you can replace some broken boards and paint the whole thing, instead. Estimating Repairs To figure out how much repairs are going to cost, we've created an article on estimating rehab costs that you might find useful. Or, alternatively, there is a "Rehab Calculator Tool" that might help (this is an affiliate link BTW where we may or may not get paid a commission).

How to make repairs

- Hiring a GC If you'd rather have a general contractor take care of everything for you and hire the right subcontractors, then this is another option. This the most expensive route but if you're BRAND new to making repairs on a house and/or you don't have time to meet with subcontractors weekly... then this might be a good choice. Make sure you communicate with your GC weekly to make sure the project is moving forward

- You're the GCIf you understand some parts of a remodel, you can go ahead and act as the GC to save that cost. You'd have to go out and find subcontractors, meet with them, and get quotes. You'd have to manage the project on a weekly basis to make sure your project is moving forward. This is less expensive than a GC but it is most time intensive, however, it's a great learning opportunity as well.

- You do some work Not a recommended avenue but you can do some of the work yourself if you know how. However, a word of wording: Don't buy a bad deal thinking: I'll just save on rehab costs by doing the work myself. This is a bad mentality. There are plenty of good deals out there. Don't put yourself in a bind like that when you don't have to.

Renting Your Brrrr Deal

The next step to making your Brrrr deal work is finding tenants. Hopefully, while you were rehabbing the property you were also "priming" your property for tenants. Sometimes it takes time to find a tenant and you can start early by getting ads up and building interest. Save those interested folks into your data base and contact them back to set viewing appointments when your rehab is complete. Managing and finding tenants, a whole book can be written on that subject. So just know that vetting a tenant is highly contingent on your state, county, and municipal laws. Find out the tenant/land lord in your area so that you don't make a big (albeit honest) mistake. A very easy way to find tenants and to make sure you're doing everything legitimately is to hire a local property manager.

Refinance Your Brrrr Deal

The step is where you get paid, and it's the "key" to making it all work. Once you get your property fixed up and you've got a tenant in the house now it's time to start shopping for a refinance loan to pull your initial capital out. Now Looking for banks

- Only work with banks that have "cash-out" refinance loans

- Only choose a bank that will cash you out immediately after you've rehabbed (they don't have a seasoning period for this

Some things to keep in mind:

- Some banks might only loan on 70%-75% of the appraised value for an investment property (which is fine because if you bought with a discount that's the majority of your investment)

- You might be able to find a bank that loans on a higher loan-to-value ratio but then you'll be paying a higher mortgage and receive less cash flow

- Banks might look at your debt-to-income ratio and credit score to make sure you can afford the loan (even though it's an investment property and the rental income covers the mortgage, they still don't see it that way for an SFR unless you're getting a "portfolio loan" or a commercial loan)

Repeat The Brrrr Method

The magic to this is that as soon as you refinance you've got almost all of your initial capital back and you can repeat the process just adding more and more cash-flowing properties to your portfolio. In fact, see this video on how Ryan Dossey, a serial entrepreneur, added 150 properties to his portfolio in under 2 years:

Other Important Thoughts

Cash flow vs Appreciation There are lots of strategies for wealth creation. Some people on forums and Youtube will preach that “appreciation” should only be an added bonus. But others that invest in highly appreciative areas like Southern California and Florida, will scoff at that and say their entire wealth strategy is built on the appreciation. Generally speaking, areas that are known to have exponential appreciation growth, are also known to have very low cash flow margins. And vice versa is true. (This is "generally" speaking. Sometimes you find places that give you a little of both).  There are untapped markets where you can find BOTH (appreciation AND cash flow), but you’d have to be researching several different markets and tap into them early. You’ll find a lot of debate on both sides of the aisle on this. It comes down to YOUR goals:

There are untapped markets where you can find BOTH (appreciation AND cash flow), but you’d have to be researching several different markets and tap into them early. You’ll find a lot of debate on both sides of the aisle on this. It comes down to YOUR goals:

- Are you looking to be financially free in a few years and have cash flow replace your current income? Then you’ll want to focus on cash flow instead of appreciation.

- Are you looking to increase your wealth? Then you’ll want to focus in on areas that have a historic record of massive appreciation (like Southern CA, and South Florida) while still making sure that the cash flow covers yearly expenses.

Negative cash flow Carrying on with the “appreciation vs cash flow” debate... There are some investors that say buying a negative cash flow property isn’t a bad thing. Because the upside is exponential appreciation on your Brrrr property. If you have a negative cash flow of -$50 per month, that’s an expense of $600 annually. But, if you have an annual appreciation growth of 10%, and the value of your property is $300,000, that’s $30,000 added every year to your equity. Of course, this can be a risky strategy (because you’re relying on the market fluxations), and many investors (especially cash flow investors) shun it… however, know there ARE investors that do use is to grow their wealth. But, do your research! Here’s a video on Michael Blank, an apartment investor, on how to buy a negative cash flow property:

Summary

To reach your your financial goals via real estate, the Brrrr strategy is a REAL and plausible method that you can use TODAY to achieve your dreams. It's literally turned people into millionaires in less than 10 years. It starts with buying right and I hope that this article was a primer for teaching you that methodology.