Agents

How To Buy Your First AirBnB Property (With No Money)

Want to earn passive income through real estate investing, specifically Airbnb properties, without a significant down payment?

In this guide, we’ll delve into how to buy Airbnb property with no money, discussing different financing options like conventional loans, FHA loans, and seller financing, as well as creative strategies like partnering with others, rental arbitrage, and house hacking. Get ready to embark on an exciting journey to unlock the potential of Airbnb investing with no money down.

Conventional loans are long-term mortgages offered by banks and other financial institutions that can be used to finance Airbnb properties. These loans are known for their security and predictability, making them a popular choice among real estate investors. Fixed-rate mortgages (FRM) and adjustable-rate mortgages (ARM) are two of the most common types of conventional home loans. They offer different advantages and disadvantages to suit different needs. The major benefit of conventional loans is their relatively lower interest rates compared to other financing options like hard money loans offered by hard money lenders. However, borrowers may be required to pay private mortgage insurance if they don’t meet certain down payment requirements.

However, conventional loans typically require a down payment of around 20%. The minimum credit score requirement for a conventional loan is generally 620, although some lenders may require a higher credit score. While the down payment requirement and credit score threshold may be higher than other financing options, conventional loans remain a viable choice for investors with good credit and some savings.

Conventional loans are long-term mortgages offered by banks and other financial institutions that can be used to finance Airbnb properties. These loans are known for their security and predictability, making them a popular choice among real estate investors. Fixed-rate mortgages (FRM) and adjustable-rate mortgages (ARM) are two of the most common types of conventional home loans. They offer different advantages and disadvantages to suit different needs. The major benefit of conventional loans is their relatively lower interest rates compared to other financing options like hard money loans offered by hard money lenders. However, borrowers may be required to pay private mortgage insurance if they don’t meet certain down payment requirements.

However, conventional loans typically require a down payment of around 20%. The minimum credit score requirement for a conventional loan is generally 620, although some lenders may require a higher credit score. While the down payment requirement and credit score threshold may be higher than other financing options, conventional loans remain a viable choice for investors with good credit and some savings.

Seller financing, also known as owner financing, is an alternative to traditional financing options that allows buyers to negotiate loan terms directly with the property owner. This arrangement can potentially bypass the need for a down payment, making it an attractive option for investors with limited funds. In seller financing, the buyer and seller agree on an interest rate, payment schedule, and other loan terms, which are documented in a promissory note.

Keep in mind, seller financing might not be the best fit for every investor or all property types. To set up seller financing for an Airbnb property, it’s crucial to:

Seller financing, also known as owner financing, is an alternative to traditional financing options that allows buyers to negotiate loan terms directly with the property owner. This arrangement can potentially bypass the need for a down payment, making it an attractive option for investors with limited funds. In seller financing, the buyer and seller agree on an interest rate, payment schedule, and other loan terms, which are documented in a promissory note.

Keep in mind, seller financing might not be the best fit for every investor or all property types. To set up seller financing for an Airbnb property, it’s crucial to:

A Home Equity Line of Credit (HELOC) is a flexible financing option that allows you to borrow against the equity in your primary residence or rental property. With a HELOC, you can access funds as needed up to a predetermined credit limit, making it a convenient solution for investors who require funds for various purposes, such as purchasing an Airbnb property, funding renovations, or covering operating expenses. Another option to consider is a home equity loan, which provides a lump sum amount instead of a revolving line of credit.

Despite its flexibility, a HELOC also carries certain risks. Borrowers who fail to repay the loan may risk losing their home. Additionally, the interest rates on HELOCs are typically variable, which can lead to fluctuations in monthly payments. Hence, a careful evaluation of the potential risks and benefits should precede opting for a HELOC as a financing option.

A Home Equity Line of Credit (HELOC) is a flexible financing option that allows you to borrow against the equity in your primary residence or rental property. With a HELOC, you can access funds as needed up to a predetermined credit limit, making it a convenient solution for investors who require funds for various purposes, such as purchasing an Airbnb property, funding renovations, or covering operating expenses. Another option to consider is a home equity loan, which provides a lump sum amount instead of a revolving line of credit.

Despite its flexibility, a HELOC also carries certain risks. Borrowers who fail to repay the loan may risk losing their home. Additionally, the interest rates on HELOCs are typically variable, which can lead to fluctuations in monthly payments. Hence, a careful evaluation of the potential risks and benefits should precede opting for a HELOC as a financing option.

Learn More About Our Handwritten Mailers Here![/caption]

Learn More About Our Handwritten Mailers Here![/caption]

Key Takeaways

- Explore financing options and creative strategies to invest in Airbnb properties with no money down.

- Stay informed of local regulations and restrictions, perform due diligence & property analysis, and plan for ownership & management.

- Leverage Propstream's suite of tools to pinpoint profitable investments.

Exploring Financing Options for Airbnb Properties

The first step towards investing in Airbnb properties with no money down is to explore various financing options.Each option has its pros and cons, and the right choice depends on your individual financial situation and goals. Conventional loans, FHA loans, and seller financing are three main financing options to consider when looking to purchase an Airbnb property without a significant down payment. Weighing the benefits and drawbacks of each option will help you make an informed decision that aligns with your financial objectives and risk tolerance. The subsequent sections will delve into the details of conventional loans, FHA loans, and seller financing, elaborating on their requirements, interest rates, and potential benefits for those investing in Airbnb properties. Understanding these financing options, including when you might need to pay private mortgage insurance, will equip you with the knowledge necessary to make an informed decision when entering the world of Airbnb investing.Conventional Loans

Conventional loans are long-term mortgages offered by banks and other financial institutions that can be used to finance Airbnb properties. These loans are known for their security and predictability, making them a popular choice among real estate investors. Fixed-rate mortgages (FRM) and adjustable-rate mortgages (ARM) are two of the most common types of conventional home loans. They offer different advantages and disadvantages to suit different needs. The major benefit of conventional loans is their relatively lower interest rates compared to other financing options like hard money loans offered by hard money lenders. However, borrowers may be required to pay private mortgage insurance if they don’t meet certain down payment requirements.

However, conventional loans typically require a down payment of around 20%. The minimum credit score requirement for a conventional loan is generally 620, although some lenders may require a higher credit score. While the down payment requirement and credit score threshold may be higher than other financing options, conventional loans remain a viable choice for investors with good credit and some savings.

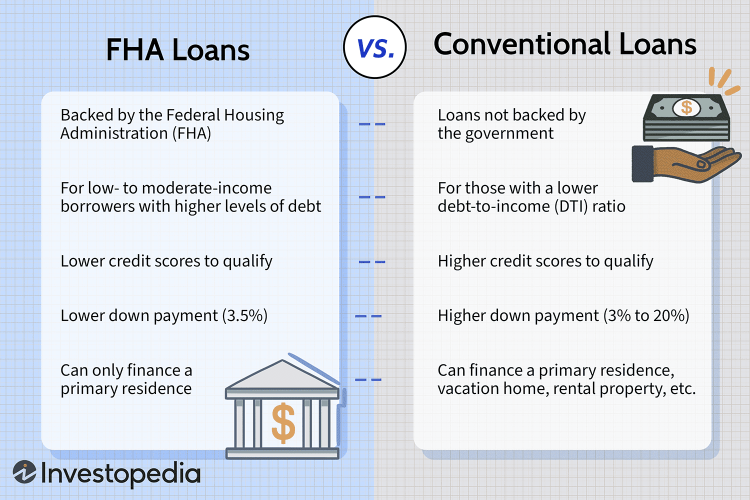

FHA Loans

Federal Housing Administration (FHA) loans offer lower down payment requirements and more lenient credit standards than conventional loans, making them an attractive option for first-time Airbnb investors. However, FHA loans are not specifically designed for Airbnb properties, as they are intended for primary residences only and cannot be used to finance second homes, rental homes, or investment properties. Additionally, FHA loan rules require the property owner to occupy the residence, with no allowance for rentals of less than 30 days. While FHA loans may not be the most suitable option for Airbnb investing due to these restrictions, they can still be a viable option for investors looking to purchase a primary residence with the intention of converting it into an Airbnb property later. In such cases, it’s crucial to research local regulations and restrictions before committing to this strategy.Seller Financing

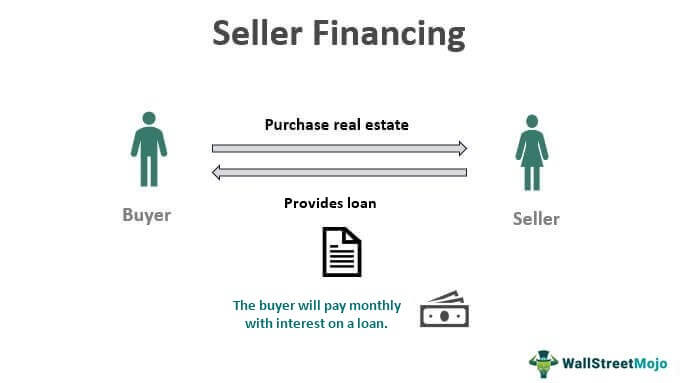

Seller financing, also known as owner financing, is an alternative to traditional financing options that allows buyers to negotiate loan terms directly with the property owner. This arrangement can potentially bypass the need for a down payment, making it an attractive option for investors with limited funds. In seller financing, the buyer and seller agree on an interest rate, payment schedule, and other loan terms, which are documented in a promissory note.

Keep in mind, seller financing might not be the best fit for every investor or all property types. To set up seller financing for an Airbnb property, it’s crucial to:

- Identify properties where the seller is open to owner financing

- Work with a real estate agent experienced in seller financing transactions

- Consult with legal and financial professionals to ensure a smooth and compliant transaction.

Leveraging Home Equity

Another approach to financing an Airbnb property with no money down is leveraging the equity in your current home or rental properties. Home equity represents the difference between the current market value of your property and the outstanding balance on your mortgage. By tapping into this equity, you can access funds to finance the purchase or renovation of an Airbnb property. Two common methods of leveraging home equity are a Home Equity Line of Credit (HELOC) and a cash-out refinance. The upcoming sections will lay out the benefits, risks, and processes tied to HELOCs and cash-out refinancing. By understanding these financing options, you can determine which method best suits your needs and financial goals.Home Equity Line of Credit (HELOC)

A Home Equity Line of Credit (HELOC) is a flexible financing option that allows you to borrow against the equity in your primary residence or rental property. With a HELOC, you can access funds as needed up to a predetermined credit limit, making it a convenient solution for investors who require funds for various purposes, such as purchasing an Airbnb property, funding renovations, or covering operating expenses. Another option to consider is a home equity loan, which provides a lump sum amount instead of a revolving line of credit.

Despite its flexibility, a HELOC also carries certain risks. Borrowers who fail to repay the loan may risk losing their home. Additionally, the interest rates on HELOCs are typically variable, which can lead to fluctuations in monthly payments. Hence, a careful evaluation of the potential risks and benefits should precede opting for a HELOC as a financing option.

Cash-Out Refinance

A cash-out refinance enables property owners to access cash by tapping into their home’s equity. This financing option involves replacing your existing mortgage with a new, larger mortgage that includes the additional cash amount. The proceeds from a cash-out refinance can be used for various purposes, such as:- Purchasing or renovating an Airbnb property

- Paying off high-interest debt

- Funding home improvements

- Covering education expenses

- Starting a business

Creative Strategies for No Money Down Purchases

If traditional financing options or leveraging home equity aren’t suitable for your circumstances, there are creative strategies for purchasing Airbnb properties with no money down. These strategies, often referred to as “airbnb with no money” approaches, include partnering with others, rental arbitrage, and house hacking. By employing one or more of these approaches, investors with limited funds can still enter the lucrative world of Airbnb investing, essentially creating an airbnb without the need for a large initial investment. The forthcoming sections will delve into each creative strategy, shedding light on their benefits, risks, and processes. By understanding these alternative methods, you can decide which strategy aligns best with your financial goals and risk tolerance.Partnering with Others

Partnering with someone who has the funds for a down payment may be able to help investors with limited resources enter the Airbnb market as a real estate deal. By sharing financial responsibility, risk management, and expertise, partners can increase occupancy rates, revenue, and the chances of a successful investment. However, partnering also comes with potential challenges and risks, such as disagreements over property management, financial disputes, and legal issues. Therefore, it’s crucial to establish a clear partnership agreement that outlines each partner’s roles and responsibilities, as well as a plan for resolving disputes.Rental Arbitrage

Rental arbitrage is a creative strategy that involves leasing a property and then subleasing it on Airbnb, potentially generating profit without owning the property. By carefully selecting properties in high-demand areas and negotiating favorable lease terms, rental arbitrage can be a lucrative option for Airbnb investing. However, there are potential legal implications and challenges associated with rental arbitrage, such as local regulations restricting short-term rentals and potential disputes with landlords. Like any investment strategy, comprehensive research and consultation with legal and financial professionals are necessary steps before undertaking the path of rental arbitrage.House Hacking

House hacking is another creative strategy for Airbnb investing that involves living in part of a property while renting out the rest. By using rental income to cover mortgage payments and other expenses, house hacking can be a cost-effective way to enter the Airbnb market. To successfully implement the house hacking strategy, investors need to:- Obtain an owner-occupied investment property loan, which typically has less stringent requirements than other loan types

- Balance the pros and cons of house hacking

- Consult a lender or financial advisor to figure out if house hacking is the most suitable choice for your situation.

Navigating Local Regulations and Restrictions

Navigating local regulations and restrictions is crucial for Airbnb investors, as rules for short term rental properties can vary by location and may impact profitability. Understanding the applicable laws and regulations in your area can help you avoid potential legal issues and ensure your Airbnb property remains compliant. To obtain information on local regulations, you can reach out to local government authorities or consult Airbnb’s local help pages. Additionally, seeking legal consultation can help ensure compliance with ever-changing regulations concerning Airbnb. By staying informed about local rules and restrictions, you can better navigate the complexities of Airbnb investing and mitigate potential risks.Finding Profitable Airbnb Investment Properties

Finding profitable Airbnb investment properties requires thorough research, market analysis, and the use of tools like Propstream to identify high-demand areas and properties with strong potential returns. By carefully analyzing market trends, occupancy rates, and comparable properties, you can pinpoint promising investment opportunities and maximize your return on investment. Propstream offers a comprehensive suite of tools, including:- Neighborhood analysis pages

- Investment property search engine

- Property Finder, which leverages AI and machine learning to suggest and compare the most profitable Airbnb rental properties in up to five markets

Learn More About Our Handwritten Mailers Here![/caption]

Performing Due Diligence and Property Analysis

Committing to an Airbnb property should be preceded by due diligence and a thorough property analysis. This process helps you assess the viability of a property, taking into account factors like rental income, occupancy rates, and return on investment. A comprehensive Airbnb property analysis typically includes:- Market research

- Performance analysis of comparable properties

- Itemization of expenses

- Assessment of time commitment

- Consideration of individualized experience

- Comprehensive real estate market analysis

Preparing for Ownership and Management

Becoming an Airbnb host involves more than just purchasing a property; it also requires understanding the responsibilities of ownership and management. As an Airbnb host, you’ll need to:- Maintain the property

- Communicate with guests

- Adhere to local regulations

- Understand tax requirements

- Obtain necessary licenses and permits

- Ensure compliance with safety regulations